Free exchange

Horns of a trilemma

How can emerging economies protect themselves from the rich world’s monetary policy?

At issue is how the flood (and ebb) of foreign capital affects economies. The traditional rule has been that countries face a “trilemma”: they must choose between free capital flows, a fixed exchange rate and an autonomous monetary policy.

“The impossible trinity” sounds like new-age theology but simply posits that an economy can choose at most two of these three. An economy open to free movement of capital can keep a fixed exchange rate, for example, only by subjugating monetary-policy goals to its defence—by raising interest rates sharply, say, when capital outflows put downward pressure on the currency. Yet the trilemma also implies that an economy can enjoy both free capital flows and an independent monetary policy, so long as it gives up worrying about its exchange rate.

Emerging-market leaders have long been sceptical of this notion. The Asian crisis led much of the developing world to abandon fixed exchange rates. Yet many emerging-market central banks still intervene in foreign-exchange markets, partly to neutralise inflows of “hot money” from rich countries. Footloose capital generates bubbles as it rushes in, some complain, only to generate crises when it later retreats home. As advanced economies opened their monetary spigots to boost ailing economies, emerging-market complaints grew louder. Some countries, like Brazil, reacted by imposing capital controls.

Mainstream economics is increasingly sympathetic. In late 2012 the International Monetary Fund updated its institutional view on capital controls, noting that more financially open economies did worse in the crisis of 2007-09. The IMF suggested that limited, co-ordinated policies to temper flows could be warranted, especially in economies with relatively underdeveloped financial systems. In a 2012 lecture Maurice Obstfeld, an economist who helped develop the trilemma concept, mused that the world’s financial architecture looked ill-prepared for a world of outsized financial flows. On average, he notes, newly industrialised economies in Asia maintain foreign-investment positions equal to 200% of annual GDP.

A new paper by Hélène Rey, of London Business School, goes further. Ms Rey reckons the trilemma itself has been rendered obsolete by financial globalisation. Governments instead face a dilemma, or an “irreconcilable duo”: free capital flows may inevitably mean a loss of monetary-policy independence.

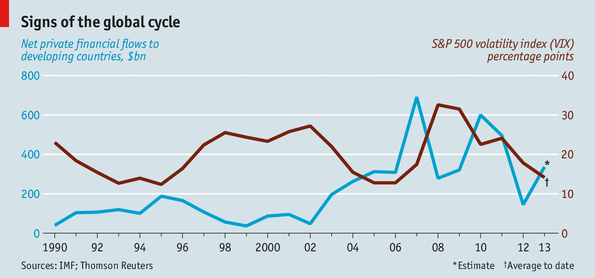

Ms Rey points out that prices of risky assets, such as equities and corporate bonds, move in lockstep across the global economy, regardless of what exchange-rate regime is in place. She links these moves to swings in the VIX—an index of market volatility derived from S&P 500 stock-options prices—which is also correlated with capital flows and credit growth. Ms Rey reckons that these movements are indicators of a global financial cycle. The worldwide correlation of price and capital-flow movements suggests that central bankers sitting in one corner of the world cannot easily lean against a barrage of investment coming from another corner.

Exactly as emerging-market finance ministers complain, this global financial cycle is influenced by rich-world monetary policy. Ms Rey reckons changes in the Federal Reserve’s benchmark interest rate can fuel the cycle. A drop in the rate increases the appetite for market risk as captured in the VIX. That, in turn, encourages credit creation, bank leverage and capital flows into risky assets. The boom feeds on itself as credit growth lifts asset prices, further whetting risk appetites. But a flip in monetary policy that raises interest rates can send the dynamic into reverse.

Fed policy is not a lone villain. Ms Rey estimates an interest-rate change can explain between 4% and 17% of variance in the VIX. Yet that may make all the difference given financial feedback loops; a small change in policy could therefore tip the system into boom or bust.

The capital-control temptation

Resolving the dilemma is not simple. Ms Rey reckons central banks

could consider spillover effects when setting monetary policy. Yet

Americans are unlikely to welcome higher unemployment at home to calm

asset prices abroad. Stronger “macroprudential” measures could be more

palatable (to individuals, if not to banks). Linking bank loan-to-value

ratios or leverage limits to economic conditions could dampen the

transmission of easy money across borders. As a last resort, capital

controls could be used. Economists generally reckon free capital flows

bring net economic benefits. But the IMF admits that the example of

countries like China, which thrive despite relatively closed capital

accounts, suggests that restrictions hardly mean certain economic doom

and gloom.India, on the wrong end of the global financial cycle, is tempted. In mid-August the government reduced the amount of money citizens could freely transfer abroad from $200,000 to just $75,000. Now may not be the time to experiment, however. Nervous investors could flee faster amid rumours of broad capital-control measures, accelerating the damage caused by the financial feedback loop. Yet the latest turn in the tide of global capital flows, and the debris it leaves behind, may tip economists’ opinion in favour of capital controls. If modest controls are the only way to secure monetary-policy independence, the trade-off may seem increasingly appealing.

Economist.com/blogs/freeexchange

No comments:

Post a Comment