Our crony-capitalism index

The party winds down

Across the world, politically connected tycoons are feeling the squeeze

It may seem that this new golden era of crony capitalism is coming to a shabby end. In London Vijay Mallya, a ponytailed Indian tycoon, is fighting deportation back to India as the authorities there rake over his collapsed empire. Last year in São Paulo, executives at Odebrecht, Brazil’s largest construction firm, were arrested and flown to a court in Curitiba, a southern Brazilian city, that is investigating corrupt deals with Petrobras, the state-controlled oil firm. The scandal, which involves politicians from several parties, including the ruling Workers’ Party, is adding to pressure on Brazil’s president, Dilma Rousseff, who is facing impeachment on unrelated charges.

A Malaysian investment fund, 1MDB, that is answerable to the prime minister, is the subject of a global fraud probe. Supporters of Rodrigo Duterte, the front-runner to win the presidential election in the Philippines on May 9th, hope he will open up a feudal political system that has allowed cronyism to flourish. In China bosses of private and state-owned firms are now routinely interrogated as part of Xi Jinping’s purge of “tigers” (a purge that has left Mr Xi’s family well alone). Worldwide, tycoons’ offshore financial cartwheels have been revealed through the Panama papers.

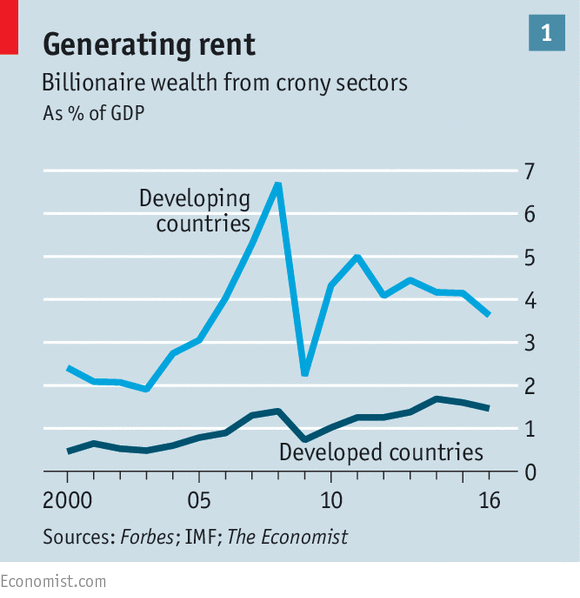

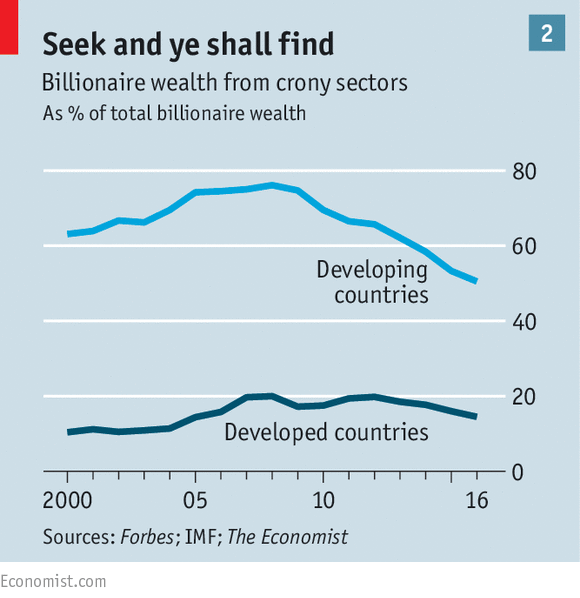

The result is that our newly updated index shows a steady shrinking of crony billionaire wealth to $1.75 trillion, a fall of 16% since 2014. In rich countries, crony wealth remains steadyish, at about 1.5% of GDP. In the emerging world it has fallen to 4% of GDP, from a peak of 7% in 2008 (see chart 1). And the mix of wealth has been shifting away from crony industries and towards cleaner sectors, such as consumer goods (see chart 2).

Behind the crony index is the idea that some industries are prone to “rent seeking”. This is the term economists use when the owners of an input of production—land, labour, machines, capital—extract more profit than they would get in a competitive market. Cartels, monopolies and lobbying are common ways to extract rents. Industries that are vulnerable often involve a lot of interaction with the state, or are licensed by it: for example telecoms, natural resources, real estate, construction and defence. (For a full list of the industries we include, see article.) Rent-seeking can involve corruption, but very often it is legal.

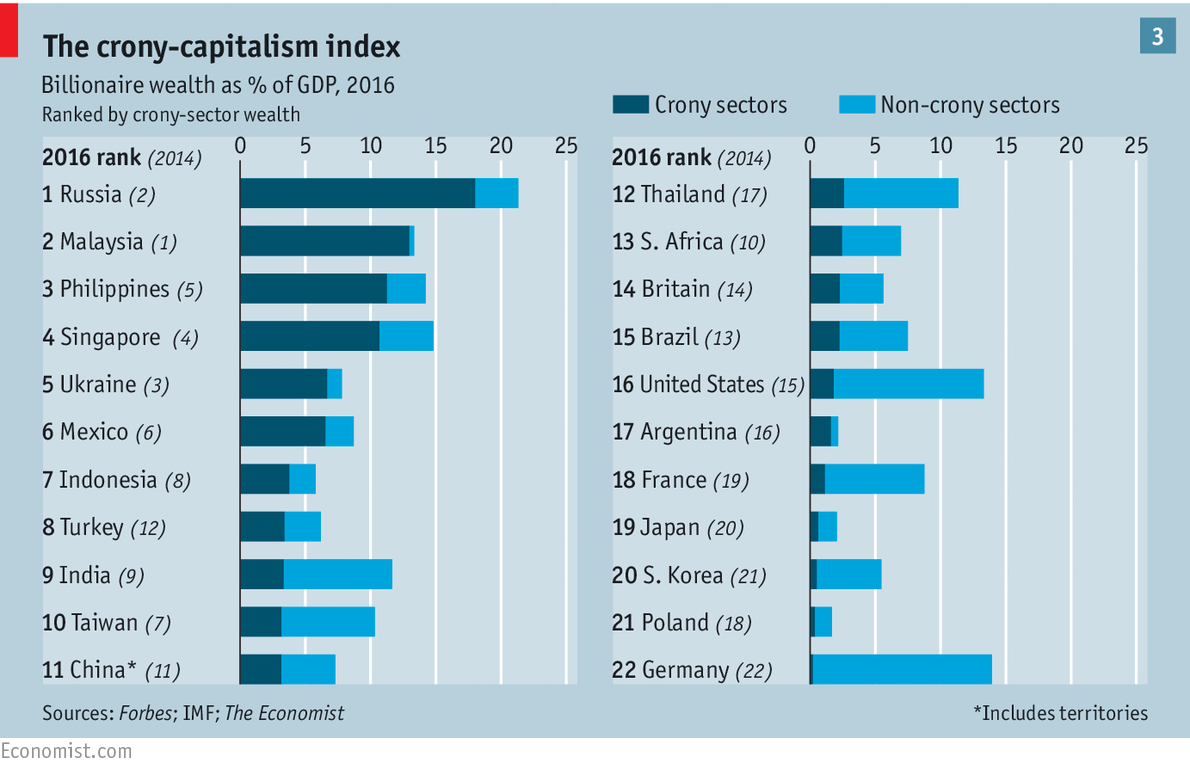

Our index builds on work by Ruchir Sharma of Morgan Stanley Investment Management and Aditi Gandhi and Michael Walton of Delhi’s Centre for Policy Research, among others. It uses data on billionaires’ fortunes from rankings by Forbes. We label each billionaire as a crony or not, based on the industry in which he is most active. We compare countries’ total crony wealth to their GDP. We show results for 22 economies: the five largest rich ones, the ten biggest emerging ones for which reliable data are available and a selection of other countries where cronyism is a problem (see chart 3). The index does not attempt to capture petty graft, for example bribes for expediting forms or avoiding traffic penalties, which is endemic in many countries.

Developing economies account for 43% of global GDP but 65% of crony wealth. Of the big countries Russia still scores worst, reflecting its corruption and dependence on natural resources. Both its crony wealth and GDP have fallen in dollar terms in the past two years, reflecting the rouble’s collapse. Their ratio is not much changed since 2014. Ukraine and Malaysia continue to score badly on the index, too. In both cases cronyism has led to political instability. Try to pay a backhander to an official in Singapore and you are likely to get arrested. But the city state scores poorly because of its role as an entrepot for racier neighbours, and its property and banking clans.

Encouragingly, India seems to be cleaning up its act. In 2008 crony wealth reached 18% of GDP, putting it on a par with Russia. Today it stands at 3%, a level similar to Australia. A slump in commodity prices has obliterated the balance sheets of its Wild West mining tycoons. The government has got tough on graft, and the central bank has prodded state-owned lenders to stop giving sweetheart deals to moguls. The vast majority of its billionaire wealth is now from open industries such as pharmaceuticals, cars and consumer goods. The pin-ups of Indian capitalism are no longer the pampered scions of its business dynasties, but the hungry founders of Flipkart, an e-commerce firm.

In absolute terms China (including Hong Kong) now has the biggest concentration of crony wealth in the world, at $360 billion. President Xi’s censorious attitude to gambling has hit Macau’s gambling tycoons hard. Li Hejun, an energy mogul, has seen most of his wealth evaporate. But new billionaires in rent-rich industries have risen from obscurity, including Wang Jianlin, of Dalian Wanda, a real-estate firm, who claims he is richer than Li Ka-shing, Hong Kong’s leading business figure.

Still, once its wealth is compared with its GDP, China (including Hong Kong) comes only 11th on our ranking of countries. The Middle Kingdom illustrates the two big flaws in our methodology. We only include people who declare wealth of over a billion dollars. Plenty of poorer cronies exist and in China, the wise crony keeps his head down. And our classification of industries is inevitably crude. Dutch firms that interact with the state are probably clean, whereas in mainland China, billionaires in every industry rely on the party’s blessing. Were all billionaire wealth in China to be classified as rent-seeking, it would take the 5th spot in the ranking.

The last tycoons

A possible explanation for the mild improvement in the index is that

cronyism was just a phase that the globalising world economy was going

through. In 2000-10 capital sloshed from country to country, pushing up

the price of assets, particularly property. China’s construction binge

inflated commodity prices. In the midst of a huge boom, political and

legal institutions struggled to cope. The result was that well-connected

people gained favourable access to telecoms spectrum, cheap loans and

land.Now the party is over. China’s epic industrialisation was a one-off and global capital flows were partly the result of too-big-to-fail banks that have since been tamed. Optimists can also point out that cronyism has stimulated a counter-reaction from a growing middle class in the emerging world, from Brazilians banging pots and pans in the street to protest against graft to Indians electing Arvind Kejriwal, a maverick anti-corruption campaigner, to run Delhi. These public movements echo America’s backlash a century ago. The Gilded Age of the late 19th century gave way to the Progressive Era at the turn of the 20th century, when antitrust laws were passed.

Yet there is still good reason to worry about cronyism. Some countries, such as Russia, are going backwards. If global growth ever picks up commodities will recover, too—along with the rents that can be extracted from them. In countries that are cleaning up their systems, or where popular pressure for a clean-up is strong, such as Brazil, Mexico and India, reform is hard. Political parties rely on illicit funding. Courts have huge backlogs that take years to clear and state-run banks are stuck in time-warps. Across the emerging world one response to lower growth is likely to be more privatisations, whether of Saudi Arabia’s oil firm, Saudi Aramco, or India’s banks. In the 1990s botched privatisations were a key source of crony wealth.

The final reason for vigilance is technology. In our index we assume that the industry is relatively free of government involvement, and thus less susceptible to rent-seeking. But that assumption is being tested. Alphabet, the parent company of Google, has become one of the biggest lobbyists in Washington and is in constant negotiations in Europe over anti-trust rules and tax. Uber has regulatory tussles all over the world. Jack Ma, the boss of Alibaba, a Chinese e-commerce giant, is protected by the state from foreign competition, and now owes much of his wealth to his stake in Ant Financial, an affiliated payments firm worth $60 billion, whose biggest outside investors are China’s sovereign wealth and social security funds.

If technology were to be classified as a crony industry, rent-seeking wealth would be higher and rising steadily in the Western world. Whether technology evolves in this direction remains to be seen. But one thing is for sure. Cronies, like capitalism itself, will adapt.

No comments:

Post a Comment