In

2015, the fracking outfits that dot America’s oil-rich plains threw

everything they had at $50-a-barrel crude. To cope with the 50 percent

price plunge, they laid off thousands of roughnecks, focused their rigs

on the biggest gushers only and used cutting-edge technology to squeeze

all the oil they could out of every well. QuickTakeFracking in Europe

Those

efforts, to the surprise of many observers, largely succeeded. As of

this month, U.S. oil output remained within 4 percent of a 43-year high.

The problem? Oil’s no longer at $50. It now trades near $35.

For

an industry that already was pushing its cost-cutting efforts to the

limits, the new declines are a devastating blow. These drillers are “not

set up to survive oil in the $30s,” said R.T. Dukes, a senior upstream

analyst for Wood Mackenzie Ltd. in Houston.

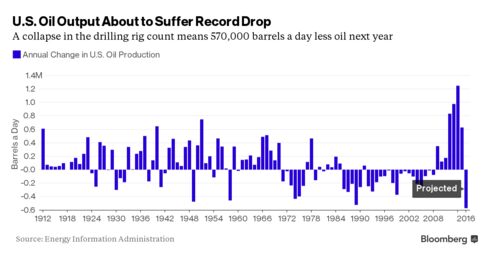

The Energy Information Administration now predicts that companies operating in U.S. shale formations will cut production

by a record 570,000 barrels a day in 2016. That’s precisely the kind of

capitulation that OPEC is seeking as it floods the world with oil,

depressing prices and pressuring the world’s high-cost producers. It’s a

high-risk strategy, one whose success will ultimately hinge on whether

shale drillers drop out before the financial pain within OPEC nations

themselves becomes too great.

Drillers

including Samson Resources Corp. and Magnum Hunter Resources Corp. have

already filed for bankruptcy. About $99 billion in face value of

high-yield energy bonds are trading at distressed prices, according to

Bloomberg Intelligence analyst Spencer Cutter. The BofA Merrill Lynch

U.S. High Yield Energy Index has given up almost all of its

outperformance since 2001, with the yield reaching its highest level

relative to the broader market in at least 10 years.

“You

are going to see a pickup in bankruptcy filings, a pickup in distressed

asset sales and a pickup in distressed debt exchanges,” said Jeff

Jones, managing director at Blackhill Partners, a Dallas-based

investment banking firm. “And $35 oil will clearly accelerate the

distress.”

Shale Rock

To understand why production is

about to collapse, we have to go back to how it came about. Geologists

have long known about shale. It’s what they called the source rock: Oil

and gas leached out of the shale into the porous dirt around it that

drillers could easily pump from. The shale itself was so impermeable

that wells would go dry almost immediately.

A wildcatter named

George Mitchell solved the problem by using directional bores to carve a

long horizontal hole through the shale layer, and then blasting that

tunnel with high-pressure bursts of water, chemicals and sand to create

millions of tiny fissures through which oil and gas could escape. It

worked, but was too expensive to implement on a wide scale.

Oil

prices rose as rapid global economic growth in the early 2000s boosted

energy demand, making shale profitable to drill. Output leaped more than

60 percent from the end of 2010.

The production burst came just

as growth slowed from its breakneck pace. As supply overwhelmed demand,

prices fell from the $100s to the $70s and then, after the Organization

of Petroleum Exporting Countries decided to keep pumping at near-record

levels, into the $30s.

“Shale is disruptive,” said Dukes. “It

brought on big volumes in a short period and eclipsed demand growth, and

the oil market began to look worse and worse.”

Spending Cuts

A

return to cheaper oil was thought to be disastrous for shale, but

companies figured out how to increase productivity and lower costs.

Producers

slashed spending, idling more than 60 percent of the rigs in the U.S.

They drilled and fracked faster, meaning fewer rigs and workers could

make the same number of wells. They focused on their best areas and used

more sand and water in the fracking process so each well gushed with

more crude. By April, when the rig count had fallen in half, output was

still rising.

All that effort did was push prices lower and

expectations for a price recovery further out into the future. Now shale

companies face a grim future, having played most of their best cards.

“There

is limited scope for further production cost reductions,” Mike Wittner,

head of oil-market research for Societe Generale, said in a note to

clients. “While technological and efficiency improvements may continue

gradually, oil company renegotiations with contractors are essentially

done, and so is the rapid shift to focus only on core areas.”

Shale

drillers aren’t the only ones hurting. OPEC’s strategy is causing pain

for its members. Saudi Arabia is said to be considering selling stakes

in state-owned companies to help stem a budget deficit that reached 20

percent of its economy. Venezuelan Oil Minister Eulogio Del Pino said

the industry is “at the door of a catastrophe” if crude production

outstrips storage capacity.

Supply Glut

Even a plunge in

U.S. output may not be enough to drain a global supply glut that has

almost 3 billion barrels of oil and products like gasoline in developed

countries’ storage tanks, according to the International Energy Agency.

The world will likely be oversupplied by about 1 million barrels a day

through the first half of next year before balancing, Jefferies LLC

analysts including Jason Gammel said in a Dec. 18 research note.

“Most

companies have gone into shrinkage mode, saying their goal is to stay

flat and make it through this market,” Raoul LeBlanc, an analyst with

IHS Inc. in Houston, said. “The current price is unsustainable.

Unfortunately, we have to sustain it for a while longer.”

ROLAND SAN JUAN was a researcher, management consultant, inventor, a part time radio broadcaster and a publishing director. He died last November 25, 2008 after suffering a stroke. His staff will continue his unfinished work to inform the world of the untold truths. Please read Erick San Juan's articles at: ericksanjuan.blogspot.com This blog is dedicated to the late Max Soliven, a FILIPINO PATRIOT.

DISCLAIMER - We do not own or claim any rights to the articles presented in this blog. They are for information and reference only for whatever it's worth. They are copyrighted to their rightful owners.

************************************

Please listen in to Erick San Juan's daily radio program which is aired through DWSS 1494khz AM @ 5:30pm, Mondays through Fridays, R.P. time, with broadcast title, “WHISTLEBLOWER” the broadcast tackle current issues, breaking news, commentaries and analyses of various events of political and social significance.

***************************************

LIVE STREAMING

http://www.dwss-am1494khz.blogspot.com

No comments:

Post a Comment