February 4 - Gold

$1251.70 down $8.70 - Silver $19.40 up 1 cent

"Reality is something you pick up like a signal. Most

people just don't have their radio on." … Anonymous

Would gold be allowed

to really break out? Would a DOW that is falling apart be allowed to

continue its downward trek, one which is bringing on the first signs of

serious concerns in the public arena?

No and no are the

answers.

Gold was stopped once

again at The Gold Cartel’s PLAN A hit time in London this morning and was

pressed on lower from there, falling to $1246 and change before the drop

was arrested. Breakout aborted. "Signal Silver" was the

predictive indicator for the zillionth time. May it be the reverse for a

change. Its price held up well today despite the pressure on gold and

quickly recovered to the unchanged level.

The DOW and friends

were called a good deal higher for their openings. This stood out because

the Nikkei was so weak again and the Chinese stock market dropped even

further. Yesterday the stock market weakness in Japan was viewed as a

contributor to our sharp drops. The latest…

Japan leads global

sell-off as jitters remain

Associated Press

By By YOUKYUNG LEE, AP Business Writer

Tuesday February 04, 2014 2:23 AM

SEOUL, South Korea

(AP) — Japan's Nikkei 225 stock average dived more than 4 percent Tuesday

as weakness in U.S. and Chinese manufacturing sent world markets sharply

lower.

Early European trading

mirrored the slide in Asian stock markets, showing investor sentiment

remained fragile as weak data from the world's two biggest economies

sparked concerns that growth could wane.

Germany's DAX drooped

1.1 percent to 9,088.62. Britain's FTSE 100 fell 0.6 percent to 6,429.07

and France's CAC 40 lost 0.5 percent to 4,085.76.

Earlier, Japan led the

slide in Asian stocks. The Nikkei tumbled 4.2 percent to 14,008.47 and is

down 14 percent over the past month. Toyota Motor Corp. sank 5.7 percent

before reporting a fivefold surge in its quarterly profit and Sharp Corp.

plunged 8.4 percent…

Before the Plunge

Protection Team became so active, the norm would have been to see further

selling in our markets, some distress selling kick in, and then perhaps a

good recovery (second time in a week this observation has been made here).

But the PPT was taking no chances any downside pressure might get out of

control and made sure we came in higher to counter weaker stock markets all

over the place.

Not much new to bring

your way today. Gold is in lockdown. While the price is not allowed to go

where it wants to on the upside yet, The Gold Cartel has been unable to

gain any downside traction with their attacks … and they seem unwilling to

press that case with their own dwindling supply of central bank physical

gold ammo.

The AM Fix was $1253.

The PM Fix fell to $1250.25.

The gold open interest

fell another 2673 contracts to 371,133, as its open interest closes in on

new multi-month lows. Silver, on the other hand, is back to encroaching on

multi-month highs. Its OI rose 1378 contracts to 147,365. This represents

nearly a 40% rise off of its lows of last year.

The dichotomy remains

baffling. The contrast between the two might be the most visible EVER. I

can only think of one explanation, and it is just a hunch. Physical gold

demand is really stressing out The Gold Cartel’s ability get the price lower.

While the bullion banks are publicly bearish with their market forecasts,

fewer and fewer of them are willing to put their money where their mouth is

these days. The "interest" in being short at these price levels

is drying up … hence the lower open interest.

We covered what JPM is

probably up to yesterday in gold, using derivatives to keep gold in check

as best they can. Silver is a bit of a different animal in that there are

not the above ground stocks available compared to gold. Simplistically, the

central banks don’t have silver in their vaults as they do gold. They have

dumped it over the past years.

So, they may have

decided they needed to play a more concerted role on the short side of the

futures market in the US to prevent silver from moving much higher. It is

possible that this very elevated silver open interest is subtly revealing a

growing stress in the silver arena. We don’t know if this is the case yet,

but we ought to find out once gold breaks its shackles and explodes to the

upside. When this occurs, JPM and cabal allies ought to be forced to cover

and the open interest should drop considerably as it does, before rising in

normal fashion as the price of silver heads for all-time highs.

Management of

perspective

* Hit gold at the obligatory

3:00 AM, 8:20 AM, and 9:00 AM MOPE points.

* Paint the tape.

* No follow-through allowed.

* Deny breakout.

* Set algos to pressure longs all day long.

* Force a close below $1255.

* Wait for idiot MSM to explain: Gold retreats as dollar gains, equities rebound

* Drain a little more physical out of the GLD, repeat as necessary.

The featured hit was

2,359 April contracts at 8:20 & 8:21 AM. Maybe Heaven can wait but

cartel rigging obviously can't. Even a +1% follow-through capping was

overly optimistic this time around. With JPM at over 60% of all gold

derivatives you wonder who is actually left to even show up on the long

side. Will the real Washington Generals please stand up?

Let's all be mindful

of NFP Friday coming up. It should be a jobs disaster, therefore all the

more reason to give gold a gooning. As of right now up is still down, white

is still black, and the word "counterintuitive" is all we are

given to explain such blatant interference.

JMc

Negative

GOFO and the silver signal

Good

morning Bill,

One month GOFO just dropped from +0.02800 on 2/3/14 to -0.00400 on 2/4/14

which is a big drop for one day. I find it interesting that GOFO goes

negative again while China is supposedly on holiday.

While

gold is down a fraction, silver and the gold stocks are up. As I type this,

GDX is up about ¼ percent and GDXJ is up 2%. GDXJ was flat yesterday even

as the stock market was really hit. In the past when the stock market gets

really hit, GDXJ would get totally trashed.

I

noticed that in Barron’s over the last two weeks that Marc Faber and Fred

Hickey both recommended the purchase of GDXJ. Not a bad day so far.

Paul

*08:15 Narrowing Treasury

spreads a sign of fading growth expectations -FT

The FT reported that the two- and 10-year bond yield spread has contracted

by about 30 bps since the start of the year, an unwelcome sign to the Fed

as growth expectations fade.

The article said that the important question is whether or not the drop in

stocks and rally in bonds represents some portfolio adjusting or reflects

fundamental concerns that recent soft economic data has not just been a

weather-related aberration. It added the 2-10 spread's reaction to upcoming

economic data should help answer that question.

* * * * *

*The yield on the 10

yr T note fell to 2.62%.

Crude oil rose 86

cents per barrel to $97.29.

The dollar rose .11 to

81.12. The euro fell .0011 to 1.3516. The pound rose .0020 to 1.6325. The

yen lost .65 to 101.65.

CARTEL CAPITULATION

WATCH

The DOW rose 72 to

15,445. The DOG gained 34 to 4031.

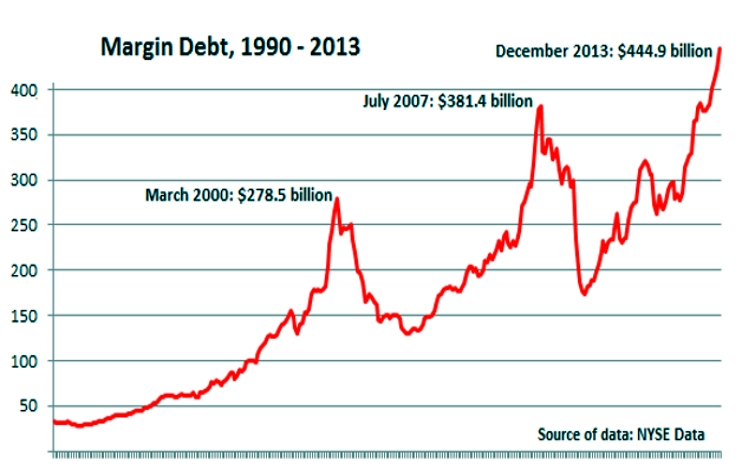

03 February 2014 NYSE Margin Debt - Take It to the

Limit, One More Time This gang

of Merry Banksters made a 1929-like policy error, as they did in 2000 for the

first crash, and then followed that up by blowing yet another asset bubble

in mortgage debt, and crashed it all over again, almost taking down the

world financial sysem.

And now they turn around and do it for a third time, with financial paper

assets. Will they keep going until the middle class and the real economy is

beaten, like pulp into the ground, and a few jokers sitting on the top of

the financial pyramid own nearly everything?

What are they thinking? Who are these guys, Mortimer and Randolph Duke?

Greenspan and Bernanke: Worst

Federal Reserve Policy, ever.

Watch the margin debt story unfold here.

Let's see what happens next.

***

10:00 Dec US Factory

Orders (1.5%) vs. consensus (1.9%)

Nov revised to +1.5% from +1.8%

* * * *

U.S. factories

expanded at much slower pace in January

Tuesday, February 04,

2014 8:48 AM

WASHINGTON — U.S.

manufacturing barely expanded last month, in part because cold weather

delayed shipments of raw materials and caused some factories to shut down.

The report from the Institute for Supply Management, a trade group of

purchasing managers, contributed to a plunge on Wall Street. The

manufacturing report raised the possibility that the U.S. economy might be

starting to weaken.

The Dow Jones industrial average tumbled 326 points — more than 2 percent.

The Dow has sunk 7 percent so far in 2014.

The ISM said Monday that its index of manufacturing activity fell to 51.3

in January from 56.5 in December. It was the lowest reading since May,

though any reading above 50 signals growth. Manufacturers said export

orders grew at a healthy pace but slightly less than in the previous month.

The figures suggest that U.S. manufacturing is slowing after a strong

finish to last year. Auto sales have decelerated, and businesses are

spending cautiously on machinery and other large factory goods. The

slowdown means that economic growth in the first three months of this year

will probably come in below the strong 3.6 percent annual pace in the

second half of 2013.

In addition, China's factory output grew at a slower pace in January, a

government report over the weekend showed. That report added to concerns

that the world's second-largest economy is weakening.

On the positive side, a measure of Europe's manufacturing sector showed

that it expanded at the fastest pace in nearly three years.

Some economists cautioned against reading too much into Monday's report on

U.S. manufacturing, given the weather impact. George Mokrzan, chief

economist at Columbus, Ohio-based Huntington Bank, said there were some

"very unusual shutdowns as a result of the cold weather" at auto

plants and other factories.

"I'd be a little bit cautious about interpreting too much from this

report," Mokrzan said. "If we don't get a bounce next month, I

would start asking deeper questions."

Monday's report showed that a measure of new orders plummeted 13.2 points

to 51.2. That is the steepest drop since December 1980. A gauge of

production also fell. Factories added jobs, the report showed, but at a

slower pace.

Bradley Holcomb, chair of the ISM's survey committee, said cold weather

affected the report in several ways. Factory closings led to lower output

and caused manufacturers to receive fewer new orders. Stockpiles of raw

materials also fell as trucking routes were closed and shipping was

delayed.

Other recent indicators have painted a mixed picture of manufacturing.

Factory output rose for a fifth straight month in December, according to

the Federal Reserve. Manufacturers cranked out more cars, trucks,

appliances and processed food.

But businesses are still spending cautiously. Orders for machinery and

other large factory goods fell in December.

DJ ISM-New York:

January Business Activity Ramps Up

Tue Feb 04 09:45:00

2014 EDT

Business activity in

the New York City area accelerated further last month as the region's

employment gauge jumped to a three-year high, according to data released

Tuesday.

The Institute for

Supply Management-New York's Current Business Conditions index rose to

64.4, from 63.8 in December and 69.5 in November. The report said that was

the first three-month streak where the reading came in above 60 in three

years. A reading below 50 indicates contracting activity.

Subindexes covering

current activity broadly improved.

The employment index

rose to its highest in three years, to 60.7 for January from 55.1 in

December. The prices-paid index increased to 63.0 from 60.0, while

purchasing volume rose to 53.8 from a neutral 50.0.

The current-revenues

index advanced to 63.5 from 60.0, while a gauge on expected revenue surged

to 71.7, its highest since August.

Only the six-month

outlook index cooled a bit to 70.0 last month, from 73.2 in December, but

still higher than any other month in 2013.

When asked about

business impediments, regulation was cited most as an issue, mentioned by

54% of respondents. A little over a third pointed to inflation as an

impediment, while 42% pointed to the cost of benefits.

Members were also

asked what factors helped to generate business opportunities. About 30%

said management skills, while 23% cited skilled labor. More than a quarter

attributed opportunities to technology.

In January's special

questions, the ISM-NY asked its members if their company expenses ran

within budget plans last quarter.

The majority, 57%,

said costs were in line with budget projections, while a quarter saw

spending running above budget and 11% below. A year ago, the exact same

proportions were reported for the last quarter of 2012.

The ISM-NY releases

its activity report, which comprises mainly non-manufacturers, one business

day before the national ISM non-manufacturing report, which is typically

released on the third business day of each month.

The national ISM

manufacturing report surprised economy-watchers Monday, when the main index

fell to its lowest since May.

U.S. IBD/TIPP economic

optimism declines to 44.9 from 45.2

U.S. IBD/TIPP economic

optimism declines to 44.9 in February

In a report,

Investor's Business Daily and TechnoMetrica Market Intelligence said their

IBD/TIPP Economic Optimism Index fell to 43.1 this month from January’s

reading of 45.2. Economists had expected the index to rise to 46.1 in

February.

A reading above 50.0

indicates optimism, while those below 50.0 point to pessimism.

The index is 0.4

points above its 12-month average of 44.5, 0.5 points above its reading of

44.4 in December 2007 when the economy entered the recession, and 4.5

points below its all-time average of 49.4.

Following the release

of the data, the U.S. dollar held on to gains against the euro, with EUR/USDshedding

0.16% to trade at 1.3507.

Meanwhile, U.S. stock

markets were higher after the open. The Dow Jones Industrial Average rose

0.35%, the S&P 500 index added 0.6%, while the Nasdaq Composite index

increased 0.55%

-END-

06:50 FT discusses

barrage of bad news that has hit emerging markets

The discussed barrage of bad news that has driven the latest bout of

emerging market turbulence. The paper highlighted the growth slowdown in

China, strikes in South Africa, political crises of varying degrees of

severity in Ukraine, Turkey and Thailand, and Argentina's devaluation. It

also pointed out that these developments have taken place against the

background of Fed tapering.

The article noted that when it comes to the potential for market

stabilization, the Institute of International Finance (IIF) seems

relatively upbeat. It said that the IIF does not believe that there will be

a sustained pullback from emerging markets. In addition, it is forecasting

a gradual rebound in capital flows in 2014 and 2015, albeit at a much lower

level to GDP than from 2010 to 2012.

However, the paper went on to highlight concerns about the negative responses

to recent tightening moves that suggest investors may be looking for even

higher rates to drive a more credible rebalancing. It also discussed the

adverse growth impact from aggressive tightening measures and the lingering

currency risk surrounding the early stages of the Fed's policy

normalization process.

http://www.ft.com/intl/cms/s/0/ddefc730-8cff-11e3-ad57-00144feab7de.html?siteedition=intl#axzz2sG1clJm6

06:00 Macro Summary:

Eurozone

ECB's Draghi is

seeking German support on bond sterilization:

Bloomberg reported

that ECB President Draghi would only consider ending the sterilization of

crisis-era bond purchases if he is openly backed by the Bundesbank,

according to two unnamed euro-area central bank officials. The article said

Draghi may ask policy makers to stop the absorption of the terminated

Securities Markets Program (SMP) if the Bundesbank sells the move to the

German public.

It noted that this

could add nearly €180B to Eurozone financial system, help to curb

volatility in money market rates and reduce banks incentive to keep cash at

the ECB rather than lend it on. It also pointed out that the ECB has failed

to fully sterilize bonds in last two weeks in a sign that banks may be

reluctant to park cash with the ECB amid tighter funding conditions.

There have also been

suggestions that the recent bond sterilization dynamic may be part of the

process of market normalization as the Eurozone emerges from crisis. In

addition, there is conjecture that some banks could be hoarding cash ahead

of the ECB's AQR. Note that the WSJ reported last Friday that despite its

typically hawkish leanings, the Bundesbank would favor an end to ECB

sterilization.

German yields fall to

six month lows: Reuters discussed the downturn in German Bund yields, which

hit the lowest levels since 5-Aug at 1.63%. It noted that the downturn in

stocks boosted demand for safe haven assets and also pointed out that

demand has accelerated since Eurozone inflation data reinforced the debate

on more ECB policy action. In addition, it discussed the speculation

surrounding ECB bond sterilization and noted this could also keep German

bond yields under pressure.

Euro may be

resurfacing as a safe haven: The WSJ reported that the euro may be

re-emerging as a safe haven currency. It noted that on some days when

emerging markets experienced a steep fall the euro has managed to rally,

which is usually a dynamic associated with JPY or USD. It discussed some of

the factors that could support the euro, including the Eurozone's large and

growing current account surplus, along with overseas demand for Eurozone

debt. It also pointed out that the ECB's low interest rate makes loans in

euros attractive and in times of stress investors that borrowed cheap money

in euros may be unwinding these bets. In addition, the article noted that

if the markets remained uncertain and the euro stayed strong then exports

would be become more expensive.

Banks/Banking

Union/Stress Tests:

European banks have

$3T of exposure to emerging markets: Reuters discussed analyst estimates

that noted European banks have loaned in excess of $3T to emerging markets,

more than four times US lenders, which puts them at greater risk if

financial market turmoil intensifies. It noted that the risk is most acute

for six European banks, BBVA, Erst Bank, HSBC, Santander and Standard

Chartered and Unicredit, which had more than $1.7T and around 12% of assets

in exposure to developing markets. In addition, it said exposure could have

an influence for the industry as a whole due to the ECB's AQR, which aims

to expose weak points and restore investor confidence in the wake of the

2008 financial crisis.

ECB's Constancio

defends strength of bank stress tests: The FT discussed yesterday's ECB

press conference, which outlined the details of its AQR and stress test

parameters. It noted comments from ECB vice-president Constancio, who said

that the exercise will be tough, demanding and very rigorous, which will

will leave no doubt over the financial system and help to boost the

Eurozone's weak recovery. Recall that the ECB said the portfolio of assets

set for inclusion in the AQR would be decided by mid-February.

ECB's Lautenschlaeger

wants swift agreement on bank failures: Reuters cited comments from ECB's

Sabine Lautenschlaeger, who urged EU negotiators to make a swift agreement

on a shared mechanism for closing down failed banks. She said that all

banks under the direct or indirect watch of the ECB's Single Supervisory

Mechanism (SSM) should fall under the joint resolution mechanism. She added

that public backstops should be in place by the time ECB starts supervising

Eurozone banks from November to ensure that any possible fallouts from the

AQR can be handled in an orderly way. She also reiterated that if possible

the period of 10 years for moving toward a single resolution fund should be

shortened.

Latest Greek data and

estimates point to a rebound: Ekathimerini discussed the latest Greek data

and estimates for the 2013 fiscal year and noted that it pointed to a

smaller-than-expected economic contraction and clear indications of a

market rebound. The rationale for this view was the primary surplus for

last year is now expected to reach €1.5B and GDP will contract less than 4%

when figures are published on 14-Feb. In addition, it expected that the

current account balance will show a surplus for 2013 and noted yesterday's

manufacturing PMI, which climbed to 51.2 in January, leaving it in

expansionary territory for the first time since August 2009.

Greece seeks deal on

Swiss secret funds to target tax evaders: Ekathimerini noted that Greek

Finance Minister Stournaras will meet with his Swiss counterpart Eveline

Widmer-Schlumpf today and Greek tax evasion will be on the agenda. The

article noted that talks on the issue have stalled since 2012 and any

progress toward an agreement would provide a boost for Greece. The report

said that Greece has vowed to clamp down on tax evasion as part of its

bailout agreement. It cited figures at the end of November, which showed

that the the country was owed €63B in unpaid taxes, fines and loans.

* * * * *

Bank of China

International hires Ex-Goldman metals chief

* Initial focus on

investor products, physical metals

SYDNEY, Feb 4

(Reuters) - Bank of China International (BOCI)

has recruited former Goldman Sachsmetals trading

chief as an adviser to help it expand its commodities business.

Chinese banks are

stepping away from mainly consumer-led business to take advantage of a

tough climate for Western brokers - grappling with strict European and U.S.

regulations - to expand their presence in natural resources, and trading in

particular.

BOCI's appointment of

Stephen Branton-Speak as an adviser is one of the highest profile metals

industry hires by a Chinese bank since Hong Kong Exchanges & Clearing

Ltd bought the London Metal Exchange (LME) for $2.2 billion in 2012.

Branton-Speak was also

on the LME board.

The initial focus of the

expansion will be on investor products and physical metals, Arthur Fan,

London-based chief executive of BOCI Global Commodities, told Reuters.

Last week, South

Africa's Standard Bank said it would sell a 60 percent stake in its

London-basedglobal markets unit to China's ICBC

for $765 million. The sale includes the metals unit of Standard Bank, a

member of the LME.

In December, a unit of

China's Shenzhen-listed GF Securities applied to trade in the LME ring. Its

local unit, GF Financial Markets Ltd, bought the commodities brokerage unit

of Natixis, including its LME ring dealing business, as the French bank

wound up its commodities broking unit.

BOCI became the first

Chinese member of the LME to much fanfare in 2012, but markets participants

have said it has failed to build on momentum.

Branton-Speak built up

Goldman Sachs' physical trading desk in the aftermath of the 2008 financial

crisis to become one of the giants on Wall Street, as banks made a bid to

offset the loss of income from the forced closure of proprietary trading

desks due to stricter regulatory reforms.

As one of the LME

executive committee members, he also played a leading part in steering the

LME's $2.2 billion sale before retiring in December of 2012.

Branton-Speak joined

Goldman Sachs in 1997 as a metals trader, before became a managing director

in 2006 and a partner in 2008. He was also on the management committee of

the London Bullion Market Association (LBMA). He is also principal

consultant with Calnic Commodity Consultancy, according to his LinkedIn

page.

-END-

06:28 Macro Summary:

China

Chinese markets remain

closed for the Lunar New Years holiday.

Jan MNI China Consumer

Indicator 95.1 (lowest since Sept) vs 97.5 prior (which was an 18-month

high)

Current conditions and future expectations both fell, with the latter

leading the decline.

Employment indicator fell sharply from an 18-month high in Dec.

Missing data may signal rising unemployment: Nikkei reported that there

were two strange developments concerning employments statistics in 2013.

The first is the unemployment rate, which dropped to 4.04% in September,

after holding steady at 4.1% since autumn 2010. It said Beijing may have

tampered with the rate to avoid problems during the party conference to

calm nerves and make the economy seem stronger than it actually is. The

other development is that the government stopped announcing the number of

jobless workers in cities. It stood at 9.18M at the end of June 2012 and

9.17M at the end of 2012, but no figures were released last year. Some

analysts suspect that the omission means there are more jobless workers

now.

China demand still

buoys global producers: The WSJ noted that China's resilient global demand

has spared many suppliers - such as tobacco farmers in Zimbabwe - even as

investors flee emerging markets. The article said a slowing China hasn't

hurt it suppliers much because massive demand hasn't significantly weakened

and many emerging economies now have their own consumers to help pick up

any slack.

China warns officials

not to cover up corruption: Reuters reported that Chinese authorities have

warned they will go after officials who cover up corruption, in the

government's latest move to curb widespread graft.

* * * * *

05:19 Macro Summary:

Japan

Nikkei continues

correction: The Nikkei closed ~4.2% lower on Tuesday, the largest

single-day loss for the index since 13-Jun. A variety of external risks

continued to weigh on the index. Weaker-than-expected data out of the US

overnight was cited as a catalyst, prompting concerns over the pace of the

US recovery. Caution surrounding emerging markets also was cited as an

overhang. It was the fifth straight negative close for the index. The

Nikkei is now down more than 14% on the year.

Amari concerned about

market overreaction: Reuters cited comments from Economics Minister Akira

Amari, who said that he was worried that investors were overreacting to US

economic data and Fed tapering. Amari cited Japanese corporate profit

growth as proof of Japan's economic revival.

Government ponders

expanding tax base to offset potential impact from cutting corporate tax:

The Nikkei reported that the Ministry of Finance is considering expanding

the tax base to offset any potential losses from cutting the corporate tax.

Recall that the government estimated that a 1% cut in the corporate tax

would decrease tax revenue by ¥470B, and that the effective corporate tax

rate will be 35.64% in fiscal 2014. The government is considering

tightening restrictions on loss carry forwards as a tool to broaden the tax

base, which would increase some companies taxable income. Also being

considered is a reduction in the exemption granted for dividend income on

entities such as subsidiaries, which would mainly target holding companies.

Muted effect of weak

yen shows hollowing-out of industrial base: The WSJ reported that exports

have not spiked as expected on a weaker yen, which the paper speculates

indicates a hollowing-out of Japan's industrial base. The article noted

that despite a 15.3% increase in the value of exports on a ~20% fall in the

value of the yen, export volumes are largely unchanged. It attributed the

lack of growth in export volume to Japanese companies moving production

overseas to hedge exchange-rate risks and weak domestic demand. There have

been a number of similar articles in recent months discussing the inability

of yen weakness to drive a pickup in export volume.

Economy:

GDP grows 0.2% m/m in

December: The Nikkei cited data from the Japan Center for Economic

Research, which revealed that seasonally adjusted real GDP was up 0.2% m/m

in December. It was the fifth consecutive month of growth. Consumer

spending increased 0.4% m/m, led by solid car sales ahead of the sales tax

increase scheduled for April. Capex declined for a second month running,

falling 0.7% m/m.

Kuroda sees 2%

inflation in late FY14/early FY15: Reuters cited comments from BoJ Governor

Kuroda, who said that Japan will experience 2% inflation at the end of FY14

or beginning of FY15. He said that Japan was "making steady

progress" towards the inflation target. Recall that when the BoJ

embarked on its QQE program, it set a 2% inflation target to be achieved

within two years. However, recently some governors have advocated extending

the two-year timeframe as they do not believe that 2% inflation is

attainable within that period.

Large Japanese

companies receive greater benefits from Abenomics: The Asahi Shimbun cited

a survey in the Diet's Lower House that revealed large companies have

received outsized benefits from Abenomics. Of respondents, 60% said that

they saw no impact or both positive and negative results, while 20% said

that they saw benefits. However 40% of large companies saw benefits,

whereas only 20% of SMEs reported seeing them. Additionally, 20% of

companies said they saw a negative impact from Abenomics, with the majority

being SMEs. Businesses biggest worry was a fall in demand following the

sales tax increase, which 34% of respondents cited, followed by increased

costs of imports including energy and raw materials, which 32% cited as the

biggest challenge that they face.

Japanese megabanks

bolstered by demand for domestic lending: Reuters cited results from

Japan's three largest banks, Mitsubishi UFJ (8306.JP), Mizuho (8411.JP),

and Mitsui (8316.JP), which all benefited from an increase in domestic

lending. Domestic loans grew 2% at the banks, the quickest since 2009, and

passed ¥200T for the first time in more than three years. The article noted

that the outlook remains bright as around 25% of Japanese companies plan to

increase capex.

Japanese megabanks

still trail big US banks in profits, market cap: The Nikkei reported that

although Japanese megabanks' earnings have outperformed, they still trail

US banks in profit and market capitalization. The article noted that US

banks profits dwarf the megabanks, and by market capitalization Japan's

largest bank ranks 14th globally. The paper attributed the relatively low

valuations to lagging profit growth, and added that Japanese banks are

looking to make overseas acquisitions to help bolster growth.

* * * * *

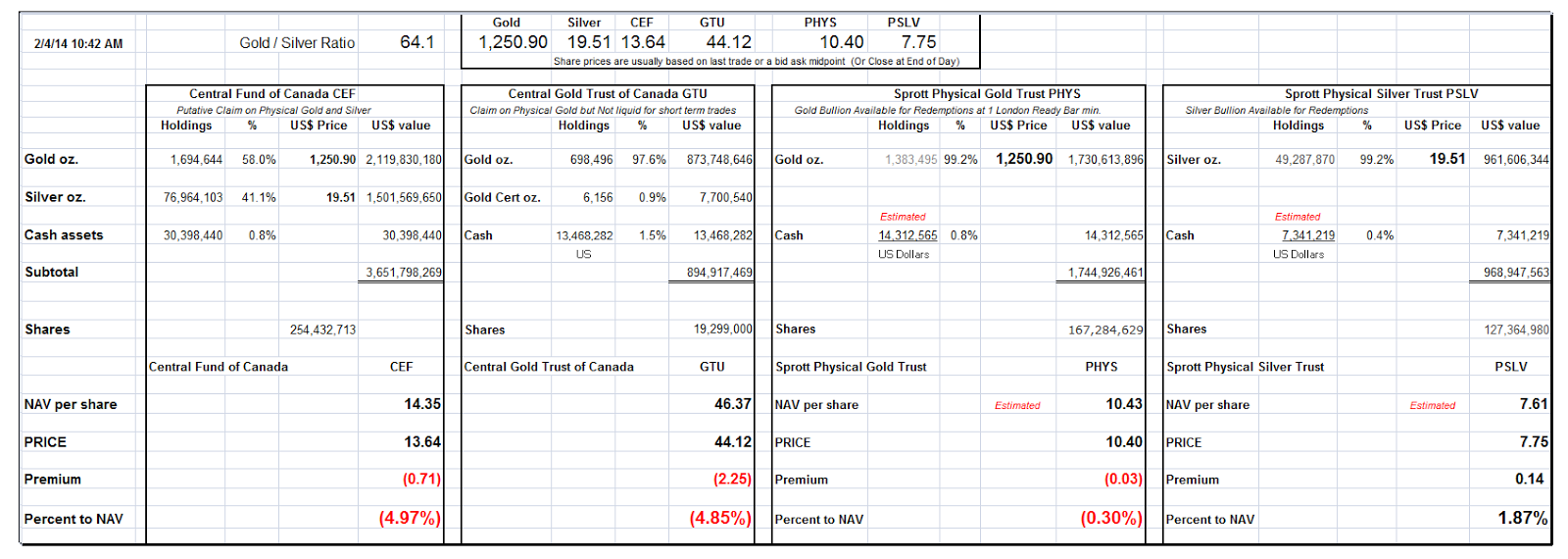

04 February 2014

NAV Premium of Certain Precious Metal Trust and Funds

- 91,680 Ounces of Gold Out of Sprott The premiums on PHYS and PSLV are back more to 'normal' levels now,

although still hardly exuberant. PSLV is at a slight premium, and PHYS is

almost flat.

The deeper discounts on CEF and GTU are still there, but a bit thinner that

they have been.

Since the

last time I

put out this chart, another 91,680 ounces of gold bullion have been

redeemed from the Sprott Physical Gold Trust.

I can imagine someone rationalizing this redemption as an arbitrage deal

because PHYS is selling at a slight discount to its NAV. However, given the

'friction' of the transaction, and the necessity of storing this amount of

gold, it seems like a fairly small amount to be tempting for a mere

arbitrage.

Although it is possible that PHYS has priced its redemption process too cheaply.

And there is no allowing for the desperation of a hedge fund that is

willing to scrape for thin returns.

But one would think that playing the spread with paper and leverage, and

betting that there would be a reversion to norms if the premiums fall to

historically low discounts, would be a smoother and more scalable wager for

any fund truly interested in paper profits.

But this seems to be viewing a phenomenon in isolation that I think it is

more correctly seen as part of a general trend, that one is foolish to

ignore.

As I have shown here repeatedly, there is a general scouring of enormous proportions of the physical

gold bullion from most if not all of the Western trusts and funds at these prices as

set by the Comex, which unfortunately is still a price maker for the

physical trade despite its own shrinking physical basis. That is the

inconvenient reality that gold imposes on the financiers: they cannot print

it into existence, except as an apparition of paper, without genuine

substance.

And there are none so blind as those whose paychecks depend on their

willing ignorance. It is unfortunate, but a fact of life.

So, let's see where this grand experiment goes. I have not been keeping an

eye on the short interest in the PHYS, but I think the greater problem is

the price of gold overall, which does not seem to be a market clearing

price in terms of the actual commodity. And as a result, the physical

bullion is flowing towards markets paying fairer prices, and finding

ownership in stronger hands.

But why argue about it? Let the tide go out, and we will see what allocated

and unallocated funds are naked. And who, at the end of the day, is

actually holding what gold, and with what encumbrances, cross claims, and

counterparty risks.

So in summary, some might say that gold is flowing out of Sprott because of

its discount to NAV, which I point out is miniscule, and much more adeptly

gamed through the usual paper games.

Rather, gold is flowing from financialised markets to cash basis markets,

from highly leveraged schemes to the vaults of stronger hands flush with

paper of less confident value, and put even more simply, from West to East.

This is what happens when once again we begin to see 'peak paper.' Yes it

certainly has not failed yet, and yes, the official measures may show

little devaluation from inflation and mask the enormous leverage and

undisclosed counterparty risk that is still in the system, après Crash.

And to this I say, 'in time.'

Not everyone is investing with a two month time horizon, as is de rigueur in the City and on

the Wall Street these days, and passing around their hot potatoes of dodgy

paper from hand to hand as quickly as possible, before the next bell rings.

***

BullionVault’s Gauge

of Client Gold Buying Falls to 18-Month Low

BullionVault, an

online service for investors to buy and sell physical gold and silver, said

its Gold Investor Index slipped to an 18-month low in January as prices

posted the first monthly advance since August.

The gauge fell to 51.9

last month, the lowest since July 2012, from 52.9 in December, the

London-based company said in an e-mailed report today. A reading above 50

indicates more buyers than sellers…

Buy while the price of

gold is still supressed - Levenstein

While the price of

gold remains suppressed, take advantage of the situation and accumulate

more gold and silver, says David Levenstein.

Author: David

Levenstein

Posted: Tuesday , 04 Feb 2014

As gold prices

continue to hover around the $1240 an ounce level, demand for the physical

metal remains extremely robust especially demand from China. Yet, despite

reports of strong demand, prices still seem to be taking the lead from

traders reacting to announcements from central banks, particularly the US

Federal Reserve and certain non-related economic news.

After gaining for most

of the month, the price of gold notched up its first weekly drop in six due

to further signs of U.S. economic growth, concerns over the U.S. Federal

Reserve's withdrawal of monetary stimulus and a slump in Chinese demand.

Last Wednesday, the US

Federal Reserve announced its’ FOMC's decision to taper its asset-purchase

program. The FOMC decided to trim its bond purchases by another $10 billion

in its first meeting of 2014. In December when the Fed announced that it

was going to taper its purchases, gold prices fell sharply. But, this time

the Fed's decision to cut down on its asset-purchase program had little

adverse effect on gold prices. Therefore, even if the Fed continues to

taper its asset-purchase program, it is unlikely to have any long-term

effect on gold.

The recently appointed

chairman of the Federal Reserve, Janet Yellen, is considered dovish, much

like former Fed chairman Ben Bernanke. Thus, Yellen may opt for additional

monetary expansion should the recovery in U.S economy falter. And, if the

Fed comes up with new monetary measures such as pegging long-term interest

rates or raising the inflation target, these measures could increase the

demand for the yellow metal as a safe-haven investment.

When Ben Bernanke took

office in 2006, the Fed had $834.6 billion in assets, the vast majority of

which were US Treasuries. The Fed now holds around $4.1 trillion in assets.

And, the balance sheet consists of toxic debt such as mortgage debt 'guaranteed'

by insolvent government agencies.

In 2006 the Fed's

capital ratio was 3.22%. But, currently as Bernanke leaves office, the

Fed’s capital ratio is just 1.34%. And it's deteriorating rapidly.

This capital ratio in

banking represents a sort of 'margin of safety'. In a severe crisis

situation, banks with a higher capital ratio are able to withstand major

financial shocks.

Three years ago, the

Fed's capital ratio was 2.17%. A year ago it was 1.82%. Six months ago it

was 1.54%. Now, it is only 1.34%. This means that the Fed would effectively

be rendered insolvent if its assets lost more than 1.34% of their value.

So, the Fed now has a razor thin margin of safety to guarantee an exploding

balance sheet, filled with what could become worthless paper.

While the policies of

the Fed may have benefited a small percentage of people owning stocks, it

has also caused prices of many basic foodstuffs to increase, and the labour

force participation rate in the US has declined to its lowest level in

decades. So apart from artificially propping up prices of equities, I

believe that Bernanke's policies have left the Fed as well as the global

financial system in a far more precarious condition than when he started.

And, unless the US economy suddenly grows at an incredible rate, which I

very much doubt, the dollar will come under more pressure during this year.

This will in turn put pressure on dollar denominated assets. The Chinese

have obviously figured this out and hence have chosen to buy as much gold

as possible…

Barrick Gold to sell

its one-third stake in Nevada mine for $86 million

Canadian Press

DataFile

Tuesday February 04, 2014 2:47 AM

TORONTO _ Barrick Gold

Corp. (TSX:ABX) says it has agreed to divest its one-third interest in the

Marigold mine in Nevada to Silver Standard Resources Inc. for $86 million .

The deal is subject to

certain closing adjustments and is expected to close in April.

Barrick has a 33.3 per

cent share of Marigold, with the other 66.7 per cent owned by the operator,

Goldcorp Inc. (TSX:G).

The divestiture is

part of Toronto -based Barrick's ongoing effort to maximize cash flow.

Barrick's share of

production at Marigold in 2013 was about 55,000 ounces of gold.

In late January,

Barrick said it was selling its interest in two mine operations in Western

Australia for AU$75 million in cash.

The sale of the

Kanowna Belle and Kundana operations to Northern Star Resources Ltd is

expected to close in March. Barrick says the price, equivalent to about

C$73.6 million , is subject to certain closing conditions…

GATA Representative

Says:

'West Cheats Suriname with Low Gold Price'

By Ivan Cairo

De Ware Tijd

Paramaribo, Suriname

Monday, February 3, 2014

Chris Powell,

co-founder of the U.S.-based Gold Anti-Trust Action Committee, accuses

Western countries and institutions of deliberately keeping the price of

gold at a low level.

The United States, the

Netherlands, Great Britain, and even the International Monetary Fund (IMF)

have been conspiring for decades to influence the international gold

market, he says.

GATA has been voicing

its conspiracy theory on how wheeling and dealing by the American

government, the Federal Reserve (the U.S. central banking system), other

Western central banks, and the IMF have deliberately created a low price

for gold and maintained that to their advantage to protect their own

national currencies.

GATA's proof for its

theory includes a 1999 IMF document kept from the public. The document

describes in detail how the gold market is manipulated and influenced to

force the price to an acceptable level. A former president of the

Netherlands central bank made reference to gold price suppression in his

memoirs, Powell says.

Unfortunately GATA has

not had any luck with its international campaign so far. Large

gold-producing nations including South Africa have not heeded its advice to

protest the unfair dealing. Even gold multinationals, which would profit

from a higher price have not protested.

Powell explains that

it all has to do with the amount of capital invested in the gold industry.

The capital comes from the international capital market, another

institution that profits from a low price of gold. "If mining

companies go public with their accusations, they might not get the funds

needed for their investment plans," he says.

Powell argues that in

the 1960s Western central banks kept the price of gold low by selling part

of their reserves. As reserves plummeted they found new methods. One

often-used method is issuing certificates for fake gold.

Recent years have seen

the creation of large quantities of fake gold, Powell says. However, the

banks never really have the gold and they would all go bankrupt if the

public started selling their certificates and demanded their gold.

Powell considers the

move by the Central Bank of Suriname to sell part of its gold reserves an

enormous blunder. The move was likely instigated by the IMF, he says. Gold

is a solid currency with much more value than some experts claim, he adds.

New Front for

Democracy and Development Party leader Carl Breevald says this is the first

time he has heard about this theory. He will ask questions about this in

Parliament. The party had questioned the sale of the gold reserves, he

says, so Powell's theory deserves closer study.

Although he is not

aware of GATA's statements and principles, Breeveld says, it would be

unwise to ignore them. That South Africa refuses to act should not keep

Suriname from trying to find out if GATA's statements are true.

Three cheers for CP!

Chris

Just to say congratulations on a great program in Suriname!

Your invitation has ,

in my opinion, promoted you to global Ambassador status for Gata, and

deservedly so.

This is a first for

Gata, but hopefully not the last.

We need Gata

Ambassadors in every country!

Of course Gata is not

yet a nation, but that is another aspect to discuss on another day.

While the global

political Tsunami towards independence is still in its infancy, (Scotland,

Catalonia, Basques.........et cetera), Gata's time may well be arriving

faster than we think.

Gata's location will

eventually be Galt's Gulch, the only question being where, or I should say

by now, which Gulch?

Best

Alan

The shares didn't pay

much attention to the gold selloff today. After a lower opening, a number of

them drifted back up. The XAU rose .63 to 90.56. The HUI went up 1.07 to

217.51. It needs to clear 225, where there is a wall of technical

resistance.

Gold has followed

silver higher in late Access Market trading. Gold last at $1254.60. Silver

last at $12.47.

Still seems to me that

in spite of all the huffing and puffing by The Gold Cartel, the price of

gold is gearing up for an explosive move to the upside.

|

No comments:

Post a Comment