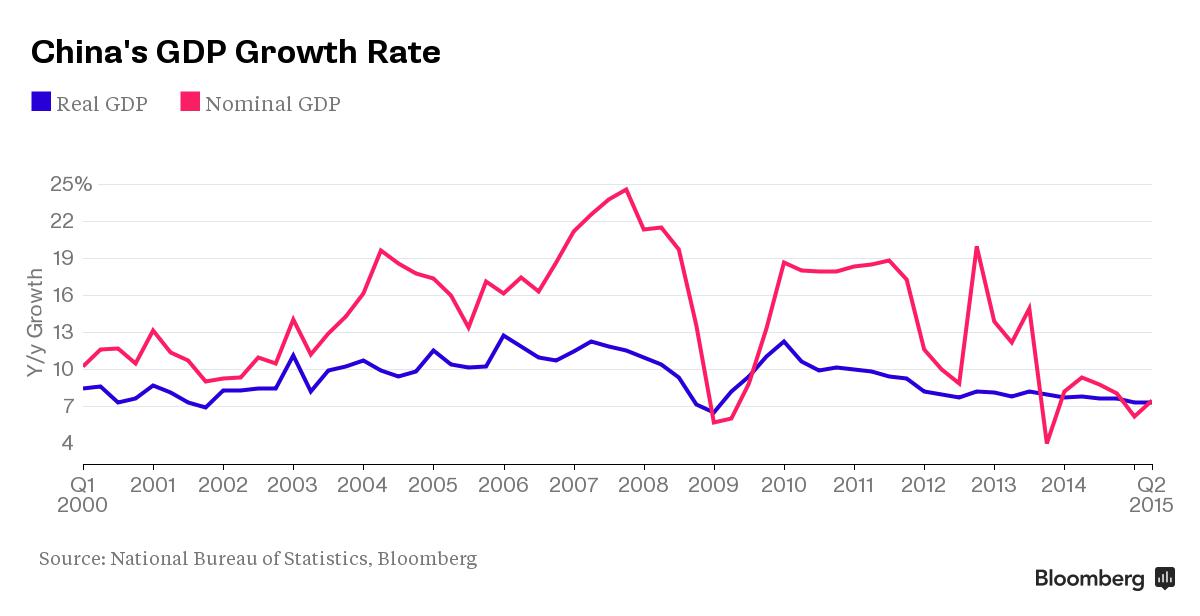

On the surface at least, China's economy grew at

a respectable 7 percent in the second quarter, beating expectations and

right on track for the government's annual growth target.

"Bingo!" was how the Xinhua official news service greeted the data in a Tweet shortly after the number was released.

But look under the bonnet and China's economy

may actually be growing much slower. When GDP is unadjusted for price

changes -- known as nominal GDP -- growth is running 2 percentage points

weaker than last year, according to data compiled by Bloomberg. On a

real basis, or when inflation is factored in, the picture looks much

better with GDP a mere half a point behind last's year's pace.

One

reason being touted to explain the gap is that China miscalculates the

so-called GDP deflator, a broad measure of prices in the economy.

Capital

Economics Ltd. argues that China's GDP deflator is underestimated in

periods when import prices are falling less than producer prices, hence

the boost to real GDP.

"It’s an esoteric point, but one with big

implications: if the deflator is understated and nominal GDP growth is

not, real GDP growth will be reported as higher than it really is," Mark Williams, Chief Asia economist at Capital Economics in London, who formerly advised the U.K. Treasury on China, said in a note.

In other words, China isn't netting out the changes in import prices when measuring overall price changes in the economy.

Skepticism

over Chinese economic data isn't new and economists frequently question

whether quarterly GDP accurately captures what's happening on the

ground.

For their part, officials from China's National Bureau of

Statistics defend their numbers and differ with the analysis by Capital

Economics.

Still, Capital Economics is standing by its analysis.

The firm agrees that China's economy may have stabilized or even

accelerated after a sluggish period, only at a much slower pace.

It

reckons that in the second quarter deflators for primary sectors like

agriculture and services rose while the deflator for secondary industry

tracked producer price inflation. And unlike the first quarter, import

prices didn't register big moves.

"We still believe there’s a

problem," Williams said in the note. "Accordingly, as in Q1, we think

that real GDP is being overestimated by one-to-two percentage points."

ROLAND SAN JUAN was a researcher, management consultant, inventor, a part time radio broadcaster and a publishing director. He died last November 25, 2008 after suffering a stroke. His staff will continue his unfinished work to inform the world of the untold truths. Please read Erick San Juan's articles at: ericksanjuan.blogspot.com This blog is dedicated to the late Max Soliven, a FILIPINO PATRIOT.

DISCLAIMER - We do not own or claim any rights to the articles presented in this blog. They are for information and reference only for whatever it's worth. They are copyrighted to their rightful owners.

************************************

Please listen in to Erick San Juan's daily radio program which is aired through DWSS 1494khz AM @ 5:30pm, Mondays through Fridays, R.P. time, with broadcast title, “WHISTLEBLOWER” the broadcast tackle current issues, breaking news, commentaries and analyses of various events of political and social significance.

***************************************

LIVE STREAMING

http://www.dwss-am1494khz.blogspot.com

No comments:

Post a Comment