Some

prominent investors are worried about China’s debt. George Soros sees

an “eerie resemblance” between conditions in China now and those in the

U.S. leading up to the financial crisis in 2008. “It’s similarly fueled

by credit growth and an eventually unsustainable extension of credit,”

Soros told the Asia Society in New York in April.

BlackRock

Chief Executive Officer Laurence Fink was asked about China’s mounting

debt on Bloomberg TV in May. “We all have to be worried about it,” Fink

said, adding that he remains bullish on China’s economy in the long run.

And

in June a Goldman Sachs report warned that the country’s large and

unaccounted-for shadow-banking activities raised concern “about China’s

underlying credit problems and sustainability risk.”

Indeed,

many segments of the Chinese economy have taken on considerable debt,

especially since the global financial crisis. Over the past decade,

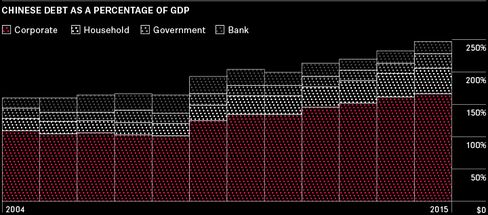

total debt grew 465 percent. Debt rose to 247 percent of gross domestic

product in 2015, from 160 percent in 2005. Bloomberg Intelligence breaks

China’s total debt into four components: bank, corporate, government,

and household. For tickers, run {CHBGDCOP Index } and then

type {DES }. Bank debt has decreased slightly in relation to

the size of the country’s economy over the past 10 years, to 19 percent

of GDP in 2015. Corporate debt, meanwhile, jumped to 165 percent of GDP

from 105 percent. Government debt rose to 22 percent of GDP. Household

debt has increased to more than 40 percent of GDP, a rise of 23

percentage points.

Despite that rapid growth,

household debt in China is far below levels in the U.S. before the

subprime crisis. At its 2007 peak in the U.S., household debt reached

almost 100 percent of GDP. What’s more, in China household savings are

twice as large as debt. Deposits were about 55 trillion yuan ($8.4

trillion) at the end of 2015, while debt was 27.4 trillion yuan.

Another

big difference between China today and the U.S. during the subprime

bubble is that Chinese residential properties are typically purchased

with significant down payments. According to the China Household Finance

Survey,

the average household debt in urban areas amounted to only 11 percent

of home value in 2012. Mortgage debt remains comparatively rare. That

showed up in the survey data: The median household debt was zero

percent. The same survey also found that if housing prices were to

decline 50 percent, less than 14 percent of mortgages would exceed the

value of the properties. Given China’s high savings rate and low

leverage, it seems unlikely that households would cause a financial

crisis.

If overwhelming debt does trigger a crisis in China, it’s

more likely the spark would come from corporations and their main

creditors, the banks. China’s bond market has shown signs of growing

stress, including 17 defaults through June 30, almost triple the number

in 2015. That and a series of delayed payments prompted rising credit

spreads and cancellations of new issues.

Leverage

problems aren’t evenly spread across Chinese corporate sectors. Energy

and materials companies have the lowest ability to service debt. Among

Chinese energy companies in 2015, the median earnings before interest

and taxes was less than one times total interest expense, according to

Bloomberg Intelligence. At materials companies, the median EBIT was

twice the interest expense. By contrast, Chinese health-care companies

have median earnings of more than nine times interest expense.

Information technology and telecommunications-services companies

generate earnings that are more than five times interest expenses. While

certain industries and enterprises have a lot of debt, Chinese

companies’ average leverage isn’t high, according to a recent

International Monetary Fund working paper.

Since 2006, listed companies that aren’t state-owned have reduced

median liabilities to 55 percent of common equity. At state-owned

enterprises, however, median leverage has been unchanged at about 110

percent. Leverage has increased at the tail end of the distribution,

driven by rising debt at companies in construction, mining, real estate,

and utilities. An increasing share of debt is attributed to a few

companies with high leverage ratios.

China

is different from other markets in an important way. Many large

corporations and nearly all the major banks are state-owned. In other

words, the debtors and creditors are ultimately owned by the same

entity. That means the country could address debt problems in some

unusual ways. One scenario is the state could take from the

prosperous—coastal regions or high tech, for example—and give to the

struggling. Another is that the government could simply cover debt. Some

unprofitable state-owned enterprises are supported by lending from

their banks essentially to keep employment at acceptable levels. Such

debts could eventually be absorbed by the state as part of its social

welfare expenditures.As China gradually opens up its stock and

bond markets, more capital could become available to deal with the

country’s obligations. The potential inclusion of Chinese stocks and

bonds in the global indexes over the next few years would help

facilitate that.

This isn’t to say that China doesn’t have some

serious problems. Growth is slowing and the economy needs major

restructuring. There will be winners and losers and turmoil in the

market. Shadow-banking activities add another risk. It isn’t certain

that the government will handle the challenges in the next decade as

deftly as it has in the past. The country’s economy is far larger and

more complex.

Fortunately for the rest of the world, China has a

high savings rate. Capital controls aren’t fully lifted, making capital

flight difficult. The government has almost complete control of the

banking industry. In addition, China’s listed banks get about 70 percent

of their funds from deposits. In comparison, U.S. investment banks in

2008 relied heavily on short-term money-market funding.

Such circumstances make it unlikely that China’s debt will spark a global crisis in the near future.

Sun is an equity market specialist at Bloomberg in Hong Kong.

ROLAND SAN JUAN was a researcher, management consultant, inventor, a part time radio broadcaster and a publishing director. He died last November 25, 2008 after suffering a stroke. His staff will continue his unfinished work to inform the world of the untold truths. Please read Erick San Juan's articles at: ericksanjuan.blogspot.com This blog is dedicated to the late Max Soliven, a FILIPINO PATRIOT.

DISCLAIMER - We do not own or claim any rights to the articles presented in this blog. They are for information and reference only for whatever it's worth. They are copyrighted to their rightful owners.

************************************

Please listen in to Erick San Juan's daily radio program which is aired through DWSS 1494khz AM @ 5:30pm, Mondays through Fridays, R.P. time, with broadcast title, “WHISTLEBLOWER” the broadcast tackle current issues, breaking news, commentaries and analyses of various events of political and social significance.

***************************************

LIVE STREAMING

http://www.dwss-am1494khz.blogspot.com

No comments:

Post a Comment